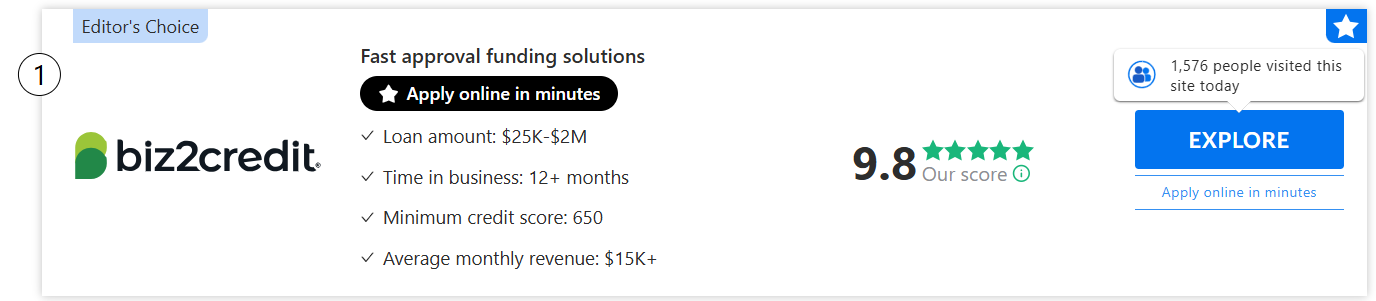

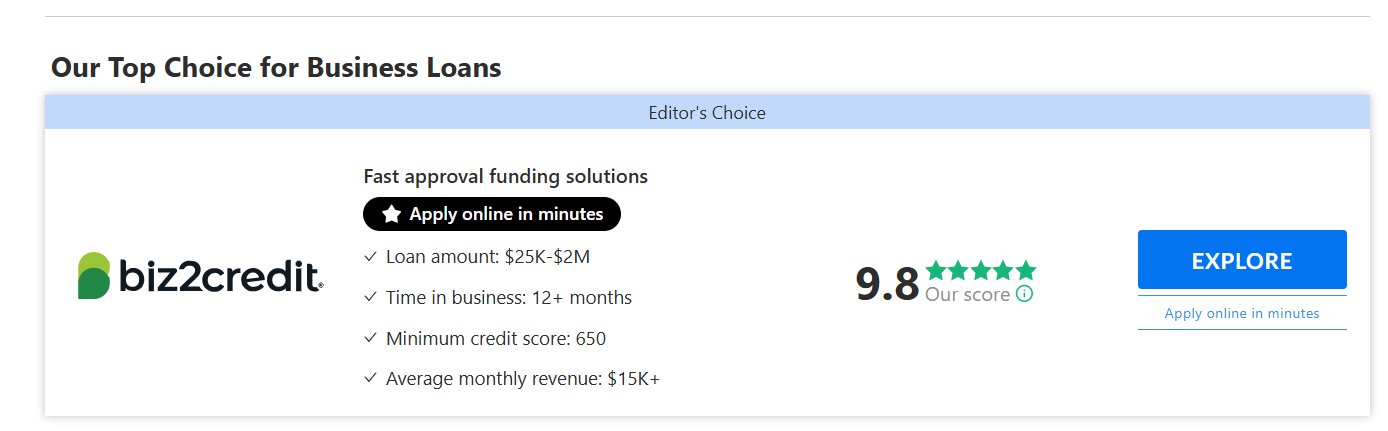

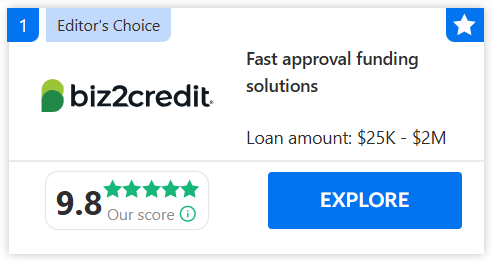

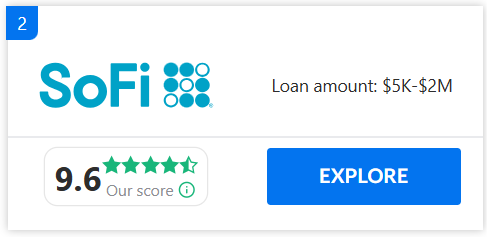

We receive advertising fees from the companies listed in the chart below, which affect rankings

We gathered and compared the best lenders out there. All you got to do is choose according to your specific needs and get a small business loan to push your business forward

Get the funding you need to enhance and grow your business

Business loans are funds borrowed by a company to meet financial needs. These needs may include covering daily expenses, managing payroll, expanding operations, or buying new equipment.

A loan provides businesses with capital they can repay over time with interest. It allows a business to move forward without waiting for savings to grow.

Banks, credit unions, and online lenders all provide business loans. The loan amount, interest rate, and repayment terms depend on the lender’s requirements and the borrower’s credit history.

For many small companies, loans are not just an option but a lifeline. They help businesses handle both planned investments and unexpected expenses.

Business loans are simple in structure. A lender provides money upfront, and the business agrees to repay it in installments with interest.

The process involves three main steps: application, approval, and repayment.

During application, lenders ask for details about the company’s financial history, revenue, and future goals. A clear business plan often increases approval chances.

During approval, lenders evaluate risk by looking at:

During repayment, the business pays back the loan through scheduled payments, usually monthly. Some short-term loans may require weekly or even daily payments.

Interest rates depend on creditworthiness and loan type. Well-established businesses often qualify for lower rates, while startups may face higher costs.

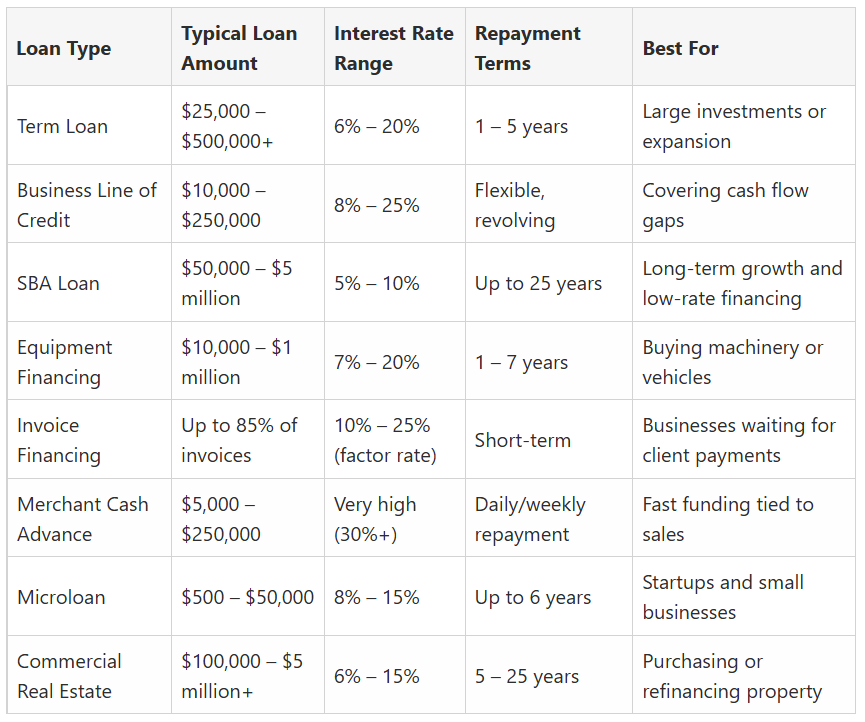

Businesses have different financial needs, so lenders offer a wide range of loan types.

These are lump-sum loans repaid over a fixed period with interest. They’re best for big expenses like office renovations, buying property, or opening a new location.

Works like a credit card for businesses. You only pay interest on the amount you use. This option is flexible for handling cash flow gaps.

Backed by the U.S. Small Business Administration, these loans come with low rates and long repayment terms. However, they require strong credit and detailed applications.

Helps businesses buy machinery, vehicles, or other equipment. The equipment itself usually serves as collateral, making approval easier.

Provides funds based on unpaid invoices. Great for companies waiting on client payments but needing cash quickly.

A lender gives a lump sum in return for a percentage of future sales. This option provides fast funding but is usually expensive.

Smaller loans, often under $50,000, aimed at startups or businesses with limited credit history. Many nonprofit lenders provide them.

Used for purchasing or refinancing business properties. Terms are often long, similar to mortgages.

Business loans can strengthen a company, but they also carry risks.

Pros

Cons

Preparation is key when applying for a loan. Lenders want to see responsibility and stability.

Steps to follow:

The application process may vary but usually includes:

Many online lenders offer quick decisions, while traditional banks may take longer but provide more favorable terms.

With many loan types available, choosing the right one requires careful thought.

Key points to consider:

Quick Tips

Business loans are a valuable tool for companies looking to grow, manage expenses, or stabilize cash flow. They provide funding for opportunities and protection during tough times.

Understanding how loans work, knowing the options available, and preparing a solid application improves the chance of approval. While loans come with risks, choosing the right lender and loan type can help businesses move forward without unnecessary strain.

By comparing lenders and reading terms carefully, business owners can find a loan that supports growth while keeping costs manageable.

Must Reads

thetopbusinesslenders.com is a free online platform designed to help users with the process of choosing the services or products that meets their needs by providing helpful reviews, articles and comparison based content. We receive compensation from the various brands we review, compare and rank on the website. thetopbusinesslenders.com is not a lender, broker or financial institute, nor a party to any engagement related to financial products or transaction. All rates, fees and offers’ terms presented herein are provided by the third party brands we engage with, which may include lenders, brokers and aggregators. We do not make any decision regarding such rates, fees, terms and eligibility or approval of a financial offer. The actual offer you will receive is subject to its provider’s sole discretion including credit score, minimum deposit, minimum balance, requested loan amount, loan term, etc. and there is no guarantee you will qualify for the rates, fees, or terms presented herein. The content herein is not, and shall not be taken as an endorsement, recommendation or solicitation to borrow or obtain any financial service. We encourage you to carefully review the actual offer’s terms you receive from the provider, including all associated fees and costs. Filing for bankruptcy shall not exempt from repayment obligations.

Annual Percentage Rate (“APR”) is the yearly cost of borrowing from a financial institution, represented as a percentage. The APR includes fees related to originating the loan, not just the interest payments (such late fees, closing fees and administrative fees). Repayment examples (for illustrative purposes only): a $20,000 loan at 6.00% APR with a term of 5 years would result in 60 monthly payments of $387 (Total repayable: $23,199) and a $100,000 loan at 3.00% APR with a term of 4 years would result in 48 monthly payments of $2,213 (Total repayable: $106,245).

thetopbusinesslenders.com is a free online platform designed to help users with the process of choosing the services or products that meets their needs by Sco providing helpful reviews, articles and comparison 590 based content. We receive compensation from the various brands we review, compare and rank on the website. The compensation we receive impacts the positioning, ranking and scoring of the brands displayed on the website. Rating or scoring we assign are based on the position in the comparison chart. The content on the website, including any reviews, ranking, rating and scoring are provided “as-is”, based solely on our team’s subjective opinion and information provided from the brand, without any warranty, including with regards to its accuracy, where each offer’s’ terms might change at any time by its provider. The listing on our website does not imply endorsement of any such brand or its products and services. We do not include or review all brands and service providers in the market. See our Terms of Use for more information.